Practical AI glossary: terms every business leader should know

This glossary defines AI terms every business leader encounters when evaluating AI adoption. ## Core AI...

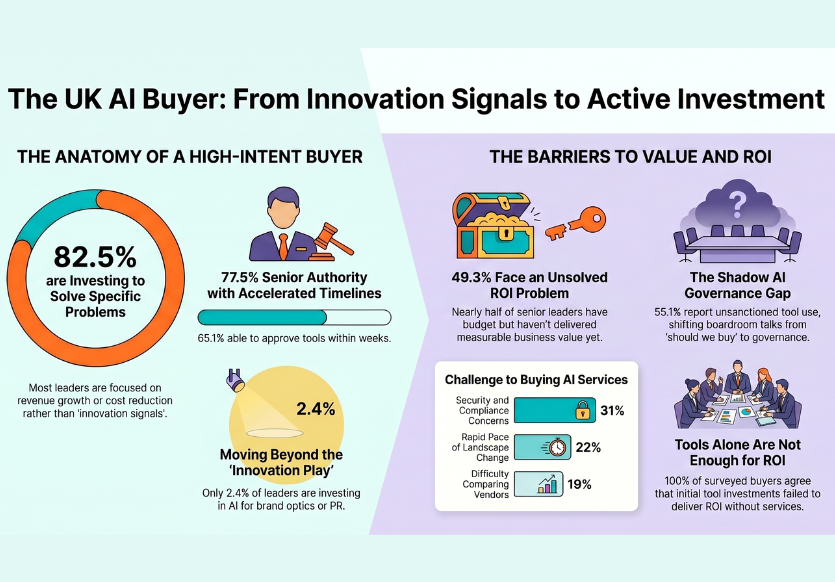

Read more82.5% of UK mid-market leaders are investing in AI to solve a defined revenue or cost problem — not to signal innovation. 65% can approve a new AI tool in days or weeks. Half currently have an unsolved AI ROI problem they are actively trying to fix. These three figures, drawn from aibl’s State of UK AI Adoption Survey 2026 (n=755), define the buyer profile inside the UK mid-market AI market in 2026.

By Richard Breeden, Founder, aibl Media Published 28 April 2026

When we set out to run The State of UK AI Adoption Research Report, we didn’t go looking for strangers. We went looking for our own audience.

The 755 people who answered our survey are the same demographic that fills our Leadership Series rooms and will fill aiblLIVE in October. UK mid-market business leaders, three quarters at C-suite, Managing Director, Owner/Founder or SVP level. The functions and sectors map almost exactly onto the people walking into our events week to week, financial services, tech and software, manufacturing, retail, operations.

So when this research tells us something about them, it’s telling us something about the room.

And what it tells us is that the room is unusually full of buyers.

82. See what 82.5% of UK mid-market leaders are investing AI in for the research behind this.5% of the leaders we surveyed are investing in AI right now to solve a defined business problem. Either driving revenue growth, or reducing operating cost. Both come with a budget attached. Both come from the operating P&L.

Only 2.4% are investing in AI to “signal innovation”m the brand play, the PR optics, the reason a lot of senior people show up to events but don’t actually buy anything when they get there.

That single split is the headline. Our audience isn’t there for the keynote. They’re there because their business has commissioned them to find a solution.

Three further numbers from the same data set fill the picture in.

77.5% of respondents are at C-suite, MD, Owner or SVP level. The rest are functional Directors, Heads and VPs. There are essentially no individual contributors in the sample. The person you actually need to talk to is already in the room.

65.1% can approve a new AI tool in days or weeks. A quarter of them (24%) can sign off in days. Just 13.5% said the approval cycle takes months. The buying window is short.

68.2% describe themselves as either “feeling the momentum, actively looking for new ways to push AI into our daily operations” or “all-in, AI as a force multiplier.” Five per cent are cautious or sceptical. The rest sit somewhere in the middle.

Stack those four signals together and 53.3% of the audience meet every criterion at the same time. 42.4% meet them at C-suite, MD or Owner level only. That is the in-market buyer cohort. It is the majority of the room.

What’s keeping these leaders awake also shows up in the numbers, and each one is a buy-trigger sitting in plain sight.

49.3% have an AI ROI problem they haven’t solved. The AI they have isn’t yet delivering measurable business value. Some are still calling it experimental. A few have been disappointed. Roughly half of the senior people in the room are walking around with a budget and a problem they haven’t worked out how to fix. That is the most direct in-market signal there is.

55.1% report that Shadow AI is common in their organisation. Their people are already using AI tools the business hasn’t sanctioned. Once that crosses a threshold, the conversation in the boardroom shifts — from “should we buy something?” to “we already have a governance gap we need to close.” That shift has a procurement consequence.

24% can approve a tool in days. A further 41% in weeks. The buying window is open now, not in the next budget cycle. That matters because most enterprise sales cycles are built on the assumption that it isn’t.

A senior operator with a problem to fix, an unsanctioned habit to formalise, and the authority to act this quarter is what an active buyer looks like. There are a lot of them in our research. There are a lot of them at our events. They are the same people.

Worth pausing on a parallel piece of research that came out a few weeks before ours.

The 2026 AI Enablement Services Buyer Survey, published by AI Enablement Insider (a 10xHumans publication) covered 100 senior decision-makers at companies between 200 and 10,000 employees, across the US, UK and Europe. All of them had already bought AI services in the previous twelve months. So this isn’t a “thinking about it” sample. It’s a sample of people who already opened the chequebook.

A few of their findings are worth quoting directly.

“78% of buyers invested in AI tools first. 100% of them say it was not enough to deliver ROI.” . The tools came first. The value didn’t follow. So the buying continued into services, training, integration, the whole stack of things that turn a tool into an outcome.

“89% of buyers say buying AI services is harder than buying other professional services.” The reasons given are practical. Security and compliance concerns at 31%. The pace of change in the AI landscape at 22%. The difficulty of comparing vendors on a like-for-like basis at 19%. Buyers want help. They struggle to find a credible way to choose between providers.

“89% expect to expand work with their existing AI vendor over the next 12 months.” Trust, once earned, gets repeat budget. The market is consolidating around a small number of providers per buyer. The window to be one of them is narrow and open right now.

Read together, our research and the 10xHumans research describe the same population from two different angles. Senior mid-market operators who have moved past the question of whether to invest. They’ve already invested. They’ve already hit the limits of what tools alone can do. They’re now actively evaluating who can help them turn that investment into something measurable.

We get asked, fairly often, what makes an aibl event a different sponsor proposition from the larger industry conferences.

The honest answer is: it isn’t the format. It isn’t the production value. It isn’t the attendee count.

It’s that the room is structurally different.

Most large-format business events are full of people who came for thought leadership, networking and brand presence. All real reasons to attend, none of which produce a buying signal. A sponsor at an event like that is paying for impressions and hoping a conversation breaks out.

Our audience is, by the data, an active buyer pool. 82.5% with an explicit business mandate. 77.5% at the level where the budget actually sits. 65% who can sign something off within weeks. Half of them with an unsolved AI ROI problem they’re trying to fix.

The line we use in sponsor conversations comes straight out of the research:

At an aibl event, 82.5% of attendees are there because their business has commissioned them to find AI solutions to a specific revenue or cost problem. 65% can approve a new tool within weeks. Nearly half currently have an unsolved AI ROI problem they’re actively trying to fix. That isn’t an audience you’re sponsoring, it’s a buyer pool you’re being introduced to.

We’re comfortable saying it because we can show the working.

If you’re a senior leader at a UK mid-market business reading this, the data also tells you something useful about yourself.

You aren’t as alone as you sometimes feel. The friction you’re working through, slow approvals, unsanctioned tools running quietly in your own teams, an ROI signal that hasn’t quite landed is the same friction the rest of your peer group is working through. Half of your peers are in roughly the same place you are.

The Leadership Series running this summer was built around exactly this. Five track: Workforce, Customer, Growth, Readiness, Efficiency each one a working session for thirty or so senior operators, not a keynote stage. aiblLIVE on 20 October 2026 brings all five tracks together at scale. Leadership Series attendees become VIP guests at aiblLIVE automatically. The path is intentional.

We are building one continuous room of people who are commissioned to act, rather than commissioned to attend.

This article is a small slice of The State of UK AI Adoption Research Report. The full version covers the five strongest predictors of measurable AI ROI, the governance maturity ladder, the workforce-training gap, the agentic-sophistication curve, and the data behind every claim above. It publishes in full this quarter.

If you’d like the full report when it lands, register for aiblBRIEF. It’s free.

How big is the aibl AI adoption survey?

The State of UK AI Adoption Research Report surveyed 755 UK mid-market business leaders between January and March 2026. Respondents were predominantly at companies with £50m to £499m annual revenue. 77.5% were at C-suite, Managing Director, Owner/Founder or SVP level.

What percentage of UK mid-market leaders are investing in AI for revenue or cost reasons?

82.5% of UK mid-market leaders surveyed by aibl are investing in AI to solve a defined business problem. 30.0% cite revenue growth, 52.8% cite cost reduction. Only 2.4% cite “innovation signal” or PR/brand reasons.

How quickly do UK mid-market businesses approve new AI tools?

65.1% of UK mid-market businesses approve new AI tools in days or weeks. 24.0% approve in days, 41.2% in weeks. Only 13.5% report “months.” Source: aibl Media, The State of UK AI Adoption Research Report, 2026.

What is Shadow AI and how common is it in UK mid-market businesses?

Shadow AI is the use of unapproved or personal AI tools by employees, outside formal IT sanction. 55.1% of UK mid-market leaders surveyed by aibl report Shadow AI is somewhat or very common in their organisation. Slow approval cycles are the leading cause.

How does the aibl audience differ from typical industry-conference audiences?

Typical large-format industry conferences attract attendees primarily for brand presence, networking and thought leadership. aibl events are populated by senior UK mid-market leaders with active mandates, fast approval cycles, and unsolved ROI problems. 53.3% of the aibl audience meets the in-market buyer triple lock — active mandate, senior decision-making authority, and a days-to-weeks approval cycle.

How do I get the full UK AI adoption research report?

The full State of UK AI Adoption Research Report publishes in Q2 2026. To register interest and receive the report when it lands, visit aiblBRIEF.

Primary source. The State of UK AI Adoption Research Report, aibl Media, 2026. Survey of 755 UK mid-market business leaders. Predominantly £50m–£499m revenue. 77.5% at C-suite, Managing Director, Owner/Founder or SVP level. Sectors covered include Financial Services, Technology and Software, Manufacturing, Retail, and Operations. Fieldwork conducted January to March 2026.

Secondary source. AI Enablement Insider — a 10xHumans publication — The 2026 AI Enablement Services Buyer Survey, March 2026. Survey of 100 senior decision-makers (Director level and above) at companies with 200 to 10,000 employees in the United States, United Kingdom, France, Germany and Italy. All respondents had purchased AI enablement services within the previous twelve months. Reproduced with attribution.

Richard Breeden is Founder & CEO of aibl Media, the UK mid-market authority on AI adoption. aibl combines proprietary research, peer-led Leadership Series events, the annual aiblLIVE conference on 20 October 2026, and the AI Enablement Directory of vetted UK delivery partners.

This glossary defines AI terms every business leader encounters when evaluating AI adoption. ## Core AI...

Read more

An AI adoption roadmap is your systematic plan for moving AI from interesting ideas to embedded business...

Read more

A governance framework is the set of policies, roles, and decision processes that keep your organisation safe...

Read moreGet ahead with the most actionable insights, playbooks and real-world AI use cases you can adopt right now, in your inbox every week